Owning and using a vehicle in a business is very complicated when it comes to determining deductible expenses for tax purposes. It involves categorizing the vehicle in the right class (luxury auto, light truck and van, SUV or other); choosing the right depreciation approach (e.g. taking bonus) and/or taking a Section 179 deduction; tracking all kinds of expenses; estimating how much the vehicle use will be for business use; determining the actual business use for the year; and finally deciding whether to use Actual Costs or Standard Mileage Rate to calculate the auto-related expenses on the tax return.

This article compares Actual Costs (including the impact of different depreciation choices) vs. Standard Mileage Rate. Since the luxury auto rules and light truck and van rules are similar, they will be combined under the broader heading of vehicles and any calculations or explanations will be done using the luxury auto rules. Before getting into specifics, here is some background information and a summary of how the rules vary by business entity type, including single owner businesses.

Background Information

Some points to keep in mind while reading through this article.

- To use the Standard Mileage Rate in future years, it must be used the first year the vehicle is put in service. Otherwise, Actual Costs must be used in all years.

- The 2019 Standard Mileage Rate is $0.59 per mile.

- The Alternative Depreciation (ADS) Straight-line method:

- Must be used if you switch from the Standard Mileage Rate to the Actual Costs method

- Must be used if Business Use percent is equal to or less than 50%

- The 2019 maximum depreciation deduction when using a MACRS depreciation method and taking the first-year bonus is $18,100.

- The 2019 maximum depreciation deduction when using a MACRS depreciation method and electing out of the first-year bonus is $10,100.

Rules by Type of Taxpayer

C Corporations and Nonprofit Corporations (aka Nonprofits)

Actual Costs: As a general rule, C Corporations (C-Corps) and nonprofits are required to use the Actual Cost method to track vehicle expenses.

Personal Use: Personal use of a company vehicle by a manager or employee is generally treated as W-2 income and there are multiple ways to determine the taxable amount.

Personal Vehicle: The Standard Mileage Rate can be used to reimburse employees for use of a personal vehicle in carrying out business for the organization. Actual expenses can also be reimbursed, but it’s likely to be more difficult to calculate. As of 2018 tax years, employees can no longer deduct company/organization-related expenses as a 2% miscellaneous itemized deduction.

S-Corporations and Partnerships

With regard to company-owned vehicles, the S-Corp or Partnership (or multiple member LLC) process works the same as for C-Corps.

Ownership: If the vehicle will be used 100% for business, then it’s fine for the S-Corp, for example, to own the vehicle. Otherwise, it’s probably better for the vehicle to be owned by the shareholder or partner.

Shareholder/Partner Personal Vehicle: The easiest approach is for the S-Corp or Partnership to reimburse the use of a personal vehicle and take a business deduction on the entity’s books for the reimbursement.

Sole Proprietors and Independent Contractors

The rules for Actual Costs vs. Standard Mileage were originally created for these types of businesses to provide an option to reduce recordkeeping. See the last Revenue Procedure published in this area in the Resources section below.

Just like many decisions, the best answer is “depends.” It depends on the circumstances for each business. For example, vehicles used 100% in the business for hauling or delivery should probably be tracked at Actual Costs. A vehicle used by the owner for both business and personal needs is when calculations and decisions have to be made.

Immediately below are some guidelines to follow when choosing between Actual Costs v. Standard Mileage, followed by examples of calculations.

When to use Actual Costs

- When the year of acquisition is the Placed-in-Service (PIS) year for a high-value car and it is bonus-eligible.

- If you or a connected person, such as a family member, used the vehicle before putting it into service in the business, it is not eligible for bonus depreciation.

- When business use is closer to 100% since this will result in a higher depreciation deduction and other expense deductions.

- When it’s likely that business use will be greater than 50% for at least 5 years; otherwise, excess depreciation taken prior to the decrease in business use would have to be recaptured as income.

- When planning to stay with the Actual Costs method. If the Standard Mileage method is not selected in the first year, then only the Actual Costs method can be used in successive years.

- When annual miles are not likely to exceed what is considered average mileage of 10,000 to 12,000 miles per year. However, this is just a rule of thumb, it depends on comparing the IRS standard mileage rate in effect for a particular year to actual costs incurred.

When to use the Standard Mileage Rate

- When placing a lower value vehicle into service.

- When you expect to drive a high number of miles in a year.

- When you expect to have a wide variance in business use over the years.

- When you have a very fuel-efficient car.

Note about electric vehicles:

Electric vehicles are very efficient, and they generally have sales prices in the range of $50,000 to $110,000. On the other hand, maintenance costs are very low. Tires, wipers and fuel costs average out to about $.05/mile. Either way, it’s a win. If the vehicle is used predominantly for business, then the depreciation deduction is high. If going with the standard mileage rate, $.59/mile is a generous reimbursement. Not to mention the potential tax credit. Qualification depends on how many vehicles the manufacturer has sold. See the link below in the Resources section below for more information.

Examples

The first example compares estimated actual costs and use for a $25,000 vehicle to the standard mileage rate. The second example shows a $60,000 purchase price. In both cases, depreciation options of bonus, no bonus and ADS straight-line are provided.

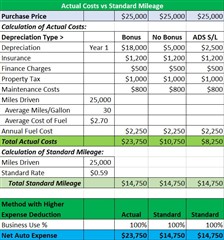

Example 1 - $25,000 Vehicle

For a $25,000 vehicle the option of taking the $18,100 bonus results in a big deduction, which would make it seem that using Actual Costs is the better approach in Year 1. The catch is that Year 2 depreciation is only $2,208 and for Year 2 the Standard Mileage method would result in the larger deduction. Unfortunately, if Actual Costs are deducted in year 1 that method has to be used for all years. (click on image to enlarge)

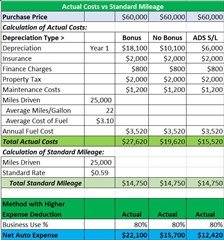

Example 2 - $60,000 Vehicle

Because of the high value of the vehicle, it seems to be advantageous to use Actual Costs for a deduction. Whereas for the $25,000 vehicle, the Actual Costs for all options only makes sense if the vehicle is driven 11,999 miles or less. For the $60,000 vehicle, with this set of facts, it would have to be driven 53,665 miles or more during the year to have the Standard Mileage Rate to be more beneficial. (click on image to enlarge)

Recommendations

Set up a spreadsheet similar to the one above and extend it out for five years or more to determine the approach that provides the most benefit.

- Input as much actual data that you have and use estimates for the rest.

- Take advantage of the multiple depreciation books available in Sage Fixed Assets—Depreciation to calculate depreciation using various methods and levels of Business Use.

- When you’re ready to enter your depreciation numbers into the spreadsheet, run the Quick Projection report to provide instant access to depreciation amounts for the life of the vehicle.

- If you were doing this ahead of a purchase, go buy the car that is the best fit both operationally and financially for your business.

- If you’re doing this analysis to determine deductions on your income tax return, be sure to involve your tax advisor to ensure that your analysis fits your specific tax situation.

Resources

KB ID: 41446 How Property Type A and T is calculated with 168 Allowance

New Safe Harbor Rules for 100% Bonus on Luxury Autos

Publication 463 (2018), Travel, Gift and Car Expenses