The Mauritius National Budget was presented by the Minister of Finance and Economic Development on 7 June 2022.

Click here to view the budget speech.

Take note: These proposed changes are subject to approval. The amended Income Tax Act is not yet available. Once enacted, the effective date for all the changes above is 1 July 2022.

Summary of the proposed changes which may affect the payroll taxes:

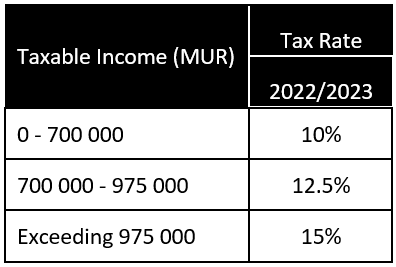

New Tax Rates

Individual earning above MUR700 000 and not exceeding MUR975 000 will now be taxed at the rate of 12.5%

Annual Tax Table

Income exemption threshold (IET)

No increase in IET for income year 2022/2023.

Deduction for tertiary education

Increase in the maximum exemption threshold to MUR500 000 for both undergraduate and postgraduate courses.

Relief for medical insurance

Increase of MUR5 000 in the maximum allowable deduction for medical insurance premiums for self and dependents as detailed below.

- Individual and his/her first dependent – Increased relief from MUR20 000 to MUR25 000.

- Each other dependent – Increased relief from MUR15 000 to MUR20 000

Deductions for donations

Maximum allowable deduction for donations made to an approved charitable institution and religious body has been increased to MUR50 000.

Travelling allowance exemption

The exemption of petrol or travelling allowances deductible from income tax will be increased from MUR 11 500 to MUR 20 000. This increase in travel allowance is applicable to all employees, irrespective of their basic salaries.

Light rail

With the introduction of light rail in Mauritius, the forthcoming amendments will clarify that workers earning a basic monthly salary of less than MUR 50 000 and who are travelling by light rail will now be able to get a refund equivalent to their relevant travelling expenses.

Personal pensions schemes

Maximum allowable deduction for contributions made to a personal pension scheme for self has been increased from MUR30 000 to MUR50 000.

Solidarity levy

An individual deriving pension or director’s fees may request the person responsible for the payment to deduct Pay As You Earn (“PAYE”) for Solidarity Levy at the rate of 10%.

Note: Software changes will be communicated in a future post.